Hugo Insurance is shaking things up in the auto insurance world with a model that’s unlike anything most drivers have seen. Instead of locking you into long-term contracts, Hugo offers short bursts of car insurance — giving you the option to pay as you go, in increments as short as just three days.

That means no big upfront costs, no deposits, and no long waits. You can activate your policy instantly and get proof of insurance in minutes — perfect for when you’re in a pinch or only need coverage temporarily.

That said, Hugo Insurance isn’t available everywhere just yet. As of now, it’s limited to 13 states, and the company only sells liability policies that meet the legal minimums. Let’s walk through what makes Hugo tick — and what you need to know before signing up.

Learn more: What is Short-Term Health Insurance?

What Is Hugo Insurance?

Hugo Insurance is a modern twist on car insurance, made for people who don’t want to deal with long-term contracts or big upfront payments. Instead of locking you into a six-month plan, Hugo lets you buy coverage in small chunks — even just a few days at a time. It’s a great fit if you drive occasionally or just need to show proof of insurance fast.

What makes Hugo stand out is how simple it is to use. You sign up online, fund your account with whatever amount you’re comfortable paying, and activate your policy right away. There’s no waiting period and no deposit required. It’s all done in minutes — no phone calls, no paperwork.

Hugo only offers liability coverage, which means it covers damage you cause to others but not your own car. If you’re looking for full protection, like coverage for accidents, theft, or weather damage, Hugo might not be enough. But if all you need is something quick and affordable to stay legal on the road, it works.

It’s currently available in 13 states, including Florida, Georgia, Ohio, and Texas. While it’s still growing, many drivers love how flexible it is — especially if you’re between jobs, sharing a car, or just don’t want to commit to a big monthly bill. Hugo gives you coverage when you need it — and lets you pause or stop when you don’t.

How Hugo Insurance Works

Right now, Hugo offers one core product: Unlimited Basic. It’s a straightforward plan that provides the legally required minimum liability insurance in 13 states — including Florida, Texas, Georgia, Ohio, Illinois, and Virginia, among others.

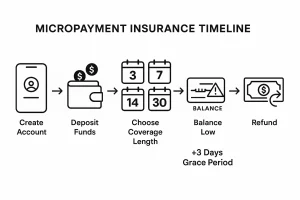

Here’s where things get interesting: You can purchase coverage for a few days at a time — three, seven, 14, 30, or even six months — depending on what fits your needs. Payments are handled in smaller increments (called “micropayments”), giving you full control over how and when you pay.

Once you create your Hugo Insurance account, you can deposit funds based on your selected plan. If your balance runs low, Hugo offers a small buffer — up to three additional days of coverage — to give you a chance to top up. You’ll need to request that extension within seven days, and once confirmed, the system will bill you for those covered days.

Keep in mind, you only have active insurance when your account is funded. If you let it lapse, you could risk penalties like registration issues or increased premiums down the road. But if you decide to stop coverage altogether, any remaining funds in your account can be refunded through Hugo’s website — no strings attached.

Pros and Cons of Hugo Insurance

Like most things in life, Hugo Insurance comes with its fair share of pros and cons. It’s a great fit for some drivers — especially those who want flexibility — but not ideal for everyone. Here’s a closer look at where Hugo shines and where it might fall short.

Pros

- Simple, No-Fuss Interface: Hugo’s platform is clean, fast, and straightforward. Signing up takes just a few minutes, and there’s no long list of forms or confusing questions. For drivers who just want to get insured quickly and move on with their day, it’s a breath of fresh air.

- Micropayments Make Budgeting Easier: Instead of charging you hundreds all at once, Hugo lets you pay in small amounts — as little as a few days at a time. That kind of flexibility is a big deal for drivers who don’t always have room in the budget for a big monthly bill.

- Same-Day Coverage: If you need insurance right now, Hugo delivers. You can get a policy active the same day — no down payment, no delays. It’s especially helpful in emergencies or for people who drive infrequently and only need short-term coverage.

Cons

- Only Covers the Basics: Hugo only offers liability insurance — the kind that protects other drivers if you cause an accident. If you’re looking for coverage that also protects your own vehicle (like collision or comprehensive), Hugo won’t be enough.

- No Full-Coverage Option: Since there’s no way to add collision or theft protection, Hugo isn’t a match if your car is leased, financed, or has high value. Most lenders won’t accept liability-only policies, so this can be a deal-breaker.

- Stopping Coverage Can Cause Trouble: While Hugo used to let drivers pause their coverage freely, that’s no longer the case. Letting your coverage lapse can lead to suspended registration or future rate hikes. It’s a flexible system — but it still requires attention.

Can You Still Turn Hugo Insurance On and Off?

Not anymore — at least, not without consequences. Hugo Insurance originally offered a Flex plan that let drivers toggle their coverage on and off as needed. But today, the only available option is the Unlimited Basic plan, which provides state-minimum liability coverage in short, manageable increments. There’s still no down payment or up-front fee, but the flexibility to pause coverage on a whim is no longer part of the deal.

Under Hugo’s current setup, turning off your insurance essentially means canceling it. And that’s not something to take lightly. If your coverage lapses, Hugo may be required to inform your state’s DMV — and in many cases, that can lead to your vehicle registration being suspended or revoked.

If you’re thinking about switching to a different policy or provider, the good news is that Hugo Insurance lets you cash out any unused balance. You can easily log into your account and request a withdrawal for any leftover funds tied to unused days.

So while Hugo still offers flexibility when it comes to how much you pay and how often, it no longer gives you the freedom to stop and start your insurance without risking penalties. If staying road-legal is important — and it should be — make sure your coverage stays active.

FAQs.

What is Hugo Insurance?

Hugo Insurance is a newer kind of car insurance — built for people who want quick, flexible coverage without all the red tape. It’s entirely online, and it lets you buy short-term liability policies that you can fund a few days at a time. There are no big deposits, no long-term contracts, and you can activate your policy in minutes. Hugo is especially helpful for drivers who don’t need full-time coverage or who want something affordable and easy to manage. Think of it as insurance that works on your schedule, not the other way around.

Does Hugo offer full coverage?

No, Hugo doesn’t offer full coverage — and that’s something to know before you sign up. The company only provides minimum required liability insurance, which is enough to meet state legal standards, but not enough to protect your own car if something goes wrong. There’s no collision, no comprehensive, and no way to bundle in extras. If your car is financed, leased, or simply worth a lot to you, Hugo’s model probably won’t cover what you need.

Does Hugo Insurance offer SR-22?

Yes, in most states where it operates, Hugo can file an SR-22 form on your behalf. An SR-22 isn’t a type of insurance — it’s a document proving that you carry the required liability coverage after a serious driving offense. You’ll need to check state availability, but many Hugo users have reported successfully obtaining SR-22 documentation through their account dashboard.

Is Hugo Car Insurance legit?

Yes, Hugo Car Insurance is 100% legit. It’s a licensed carrier, and while it’s relatively new, it has gained attention for offering instant coverage, no upfront costs, and user-friendly service. Just keep in mind: it’s liability-only, and not available in every state — but it’s fully compliant where offered.

How does Hugo Insurance work?

Hugo works differently from traditional insurers. You create an account, fund it with however much coverage you want (starting with just 3 days if you like), and activate your liability policy immediately. Payments are flexible — no big upfront bill. If your balance runs low, you can top up, and Hugo will even give you a short grace period. Coverage ends when funds run out, and you can cancel or pause anytime. Everything’s handled online, fast and simple.

Does Hugo Insurance cover Georgia?

Yes, Hugo Insurance is available in Georgia. Drivers in the state can purchase Hugo’s Unlimited Basic plan, which meets Georgia’s minimum liability coverage requirements. You’ll also get instant proof of insurance and access to Hugo’s flexible pay-as-you-go system.