Falling behind on debt isn’t just a numbers problem — it’s a mental and emotional burden. The stress builds when the phone rings with another collection call or when the interest on your credit cards keeps stacking faster than your paycheck. It’s exhausting, and it can make even the simplest financial goal feel out of reach. If you’re nodding along, you’re not the only one in this boat — and there are ways to get your head above water.

One path many people consider is debt settlement, and National Debt Relief is one of the more visible names out there. Their goal? To talk directly with your creditors and try to reduce what you owe, so you can pay less than the full amount and move forward.

It can be a huge relief — but it’s not without trade-offs. Going this route will likely hurt your credit score (sometimes by 100 points or more), at least for a while. You’ll also want to watch for added fees, potential tax implications on forgiven debt, and late penalties that might sneak in before your settlements are finalized.

Still, if you’re sitting on $7,500 or more in unsecured debt and feeling like there’s no way out, this could be a practical step toward breathing room — especially if rebuilding credit later feels easier than staying stuck now.

Here’s what you should know at a glance:

- Type of Service: Debt settlement (not a consolidation loan)

- Minimum Debt Requirement: $7,500 in unsecured debt

- Fees: Typically 18%–25% of enrolled debt (varies by state)

- Impact on Credit: Temporary drop — possibly over 100 points

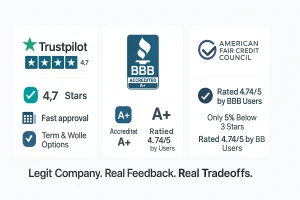

- Reputation: A+ rating from the Better Business Bureau (BBB)

Here are some more reviews for you:

- Banner Life Insurance Review

- AAA Life Insurance Review

- Ethos Life Insurance Review

- Gerber Life Grow-Up Plan Review

How National Debt Relief’s Program Works

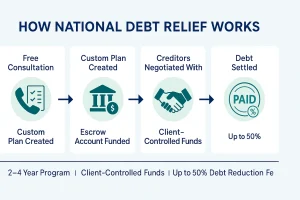

National Debt Relief doesn’t jump straight into negotiating with your creditors. First, they take a close look at your credit history and total debt to see if you qualify. There’s no hard minimum credit score required, but not all debts are eligible. The program is only for unsecured debts — think credit cards, medical bills, or personal loans. Mortgages, auto loans, and other secured debts aren’t part of the deal.

If you’re eligible, the next step is setting up a dedicated escrow account. This is where you’ll deposit money every month — and only you can touch it. NDR won’t begin talks with your creditors until there’s enough in that account to start making realistic offers. In most cases, that’s about 25% of the total debt you owe.

That money doesn’t go to NDR. It’s used to pay off your creditors once a deal is made. Ideally, they settle for less than you originally owed — and that’s where the savings come in. But it does mean you’ll be making regular payments for a while. Most people complete the program in about 24 to 48 months, depending on how much they owe and how much they can afford to set aside each month.

One thing to know: NDR typically asks you to stop paying your creditors while negotiations are happening. That move can (and usually will) hurt your credit score. But if you’re already behind and struggling, the long-term trade-off might be worth it — especially if National Debt Relief really can reduce what you owe by up to 50%, as they claim.

National Debt Relief Eligibility & Requirements

You don’t need a perfect credit score — or any specific score at all — to qualify for National Debt Relief. What really matters is the type and amount of debt you’re carrying. To be eligible, you’ll need at least $7,500 in unsecured debt, like credit cards, personal loans, or medical bills. Mortgages, car loans, and other secured debts aren’t covered under this program.

Another key part of qualifying is your ability to start making deposits into a special escrow account. This account is set up in your name, and it’s where you’ll slowly build the funds that will eventually be used to settle your debts. Think of it as your negotiation pool — once it reaches a certain amount (usually around 25% of your enrolled debt), National Debt Relief can begin talking to creditors on your behalf.

This money doesn’t go to NDR. When a deal is struck, your escrow funds are used to pay off the agreed-upon amount directly to your creditors. The more debt you’re settling, the more you’ll need to have saved in the account to move things forward. So while there’s no formal credit check hurdle, you will need a bit of upfront financial breathing room to get started.

Key Features of National Debt Relief

Debt Settlement Services

Getting started with National Debt Relief begins with a no-cost consultation. You’ll speak with a specialist who takes the time to understand where you stand — how much debt you have, what types of accounts are involved, and what your monthly budget allows. From there, they’ll outline a plan that makes sense for your specific situation, not just hand you a generic solution.

If you choose to enroll, you’ll stop making payments directly to your creditors and begin depositing money into a separate, FDIC-insured escrow account that you control. This account acts as your savings pool for eventual settlements, and the monthly amount you put in is often less than what you were trying to cover across multiple bills.

Once you’ve saved up a bit — and after your accounts have gone a few months without payments — that’s when National Debt Relief starts reaching out to your creditors. Their job is to negotiate a lower payoff or better terms on your behalf.

Debt Reduction

While nothing is guaranteed, National Debt Relief claims that many of its clients see their enrolled debts reduced by around 50% before fees. If a creditor agrees to settle, they’ll share the offer with you. If you give the green light, the money comes out of your escrow account — either as a lump sum or spread out in payments, depending on the deal.

This isn’t a one-and-done solution. Each account goes through this process individually, and the full program usually runs anywhere from two to four years, depending on how much debt you have and how steady your deposits are.

It’s not an instant fix, and it does require patience. But for those buried in debt with few good options left, it can offer a way forward — one step at a time.

Fees for National Debt Relief’s Services

Like most services that help you settle debt, National Debt Relief does charge a fee — usually between 18% and 25% of the total amount you enroll. If you’re bringing $20,000 of debt into the program, that means you’ll likely pay somewhere between $3,600 and $5,000 by the time all is said and done.

These fees aren’t paid upfront. They’re rolled into your monthly payments and only charged after a settlement has been reached and approved by you. In some states, you might also see a small extra charge for processing or servicing — but nothing should ever catch you off guard.

It’s also worth noting: federal law has your back here. Since 2010, debt settlement companies have been banned from collecting any fees before doing the work. So if a company asks for your payment info before even confirming that you’re eligible — that’s your cue to walk away.

Pros & Cons of Debt Settlement with National Debt Relief

When you’re buried under a mountain of credit card bills and overdue notices, even breathing can feel hard. For folks in that situation, National Debt Relief offers a glimmer of hope — a chance to settle what you owe for less than the full amount. In many cases, they claim to help reduce your debt by up to 50%. It’s not a magic cure, but for some, it’s the kind of lifeline that can keep you from falling deeper.

Of course, this kind of relief doesn’t come without strings. Anytime you settle a debt for less than you owe, it gets flagged on your credit report. It’s not as damaging as bankruptcy, but it’s not invisible either — that mark can stick around for seven years and might affect future borrowing.

That said, there are meaningful upsides. National Debt Relief has earned an A+ rating from the Better Business Bureau, and many people say the constant calls from collectors finally stop once they enroll. That alone can bring real peace during a stressful chapter. And if you qualify, you could see a sizable portion of your debt go away — something that might feel completely out of reach right now.

Still, this path isn’t without its risks. The amount of debt that’s wiped out might be counted as taxable income by the IRS, so you could get hit with a bill you didn’t see coming. There’s also no guarantee your creditors will play ball. And if they don’t, you’re stuck — sometimes worse off than before. On top of that, National Debt Relief’s fees range from 18% to 25% of the debt you enroll, which can eat into your overall savings. You’ll also need at least $7,500 in unsecured debt to qualify, and things like mortgages or car loans are off the table.

Is National Debt Relief Right for Me?

Debt settlement isn’t a quick fix — it’s a calculated risk. For the right person, it can be a game changer. But it’s important not to get swept away by the promise of savings without understanding the trade-offs that come with it.

National Debt Relief tends to be a better fit for people who are carrying more than $7,500 in unsecured debt — things like credit cards, medical bills, or personal loans — and who’ve already tried other ways to manage their finances without success. It’s often considered a final step before bankruptcy, and for some, a better alternative to it.

If you’re not actively paying off your debt, interest and late fees are probably snowballing already. Your credit score might be slipping, and stress levels likely rising. Settling your debt won’t magically erase those problems, but it can give you a plan — and eventually, some breathing room.

Let’s put it into perspective. Say you owe $10,000. If National Debt Relief negotiates that down to $5,000, that sounds like a big win — until you break down what’s left after the dust settles. If you’re in the 24% tax bracket, the IRS will expect $1,200 in taxes on the forgiven amount. Then factor in NDR’s fee — up to 25% of your enrolled debt, or $2,500 in this case. That leaves you with around $1,300 in actual savings.

Now ask yourself — is $1,300 worth the hit to your credit report and the stress of the process? For smaller balances, maybe not. But the story shifts when you’re dealing with bigger numbers.

Take someone with $60,000 in debt. If NDR cuts that in half, you’re looking at $30,000 forgiven. Even after paying fees and taxes, you could still walk away having saved $12,000 or more. That’s significant — and for many, it’s the break they need to finally get ahead.

So is National Debt Relief right for you? That depends on your debt size, your financial goals, and whether peace of mind today outweighs a temporarily bruised credit score. The bigger the debt, the more this path can make sense.

Alternatives to National Debt Relief

National Debt Relief might be the right fit for some, but it’s not the answer for everyone. If the thought of taking a credit score hit or losing a chunk of your savings to fees makes you hesitate, you’re not alone. The upside? There are other routes that could make more sense for your situation.

Debt Management Plans

Think of this as a structured way to get back on track without having to bargain down what you owe. A debt management plan — or DMP — involves working with a nonprofit credit counselor who bundles your unsecured debts into one affordable monthly payment. Instead of wiping out part of your debt, you agree to repay it in full over three to five years. The benefit? Creditors often agree to drop interest rates or forgive late fees. And because you’re still honoring your full balance, your credit report won’t take as big of a hit compared to settling for less.

Settling Debts on Your Own

You can also go the solo route. If you’re comfortable making tough phone calls and negotiating under pressure, DIY debt settlement might work. This means contacting your creditors, explaining your financial strain, and offering to pay part of what you owe in exchange for closing the account. Be ready to show proof — they won’t take your word alone. Your credit will still take a hit, and forgiven debt is still taxable, but you won’t owe extra fees to a settlement firm.

Freedom Debt Relief

Freedom Debt Relief is a name that comes up often in the debt settlement world. Like National Debt Relief, they negotiate with your creditors on your behalf. What sets them apart is that they offer additional support, such as credit counseling. If you want someone to walk with you, not just handle the numbers, this may be a better fit.

National Debt Relief Reputation & Consumer Reviews

When it comes to National Debt Relief’s reputation, the feedback is a bit of a mixed bag. Some folks feel frustrated by how hard it is to get clear answers upfront — especially when it comes to fees or taxes. You often have to hand over personal details or go through a soft credit check just to get a glimpse of what’s offered. A few former clients say they felt blindsided, particularly when they learned how much the company would take in fees, or that they’d owe federal income tax on the forgiven debt. At the core of most complaints? Miscommunication and unmet expectations.

That said, not all reviews are negative. In fact, the company holds a solid 4.7 out of 5 stars on Trustpilot, with more than 41,000 reviews — and only a small fraction (about 5%) fall into the three-star-or-lower category. The most common gripes in those less enthusiastic reviews tend to focus on the length of the settlement process, the final savings being less than expected, and frustration over how fees are structured.

On a more official note, National Debt Relief is accredited by both the Better Business Bureau (BBB) and the American Fair Credit Council. It carries an A+ BBB rating and a customer review score of 4.74 out of 5 across thousands of reviews. That shows there’s a large base of customers who did find relief — even if the road there wasn’t perfect.

Ultimately, National Debt Relief is a legitimate company offering a real solution to serious debt. But that doesn’t mean it’s a shortcut. You’ll need to weigh the full cost — including potential tax implications, the impact on your credit report, and the patience required. It’s not instant, and it’s certainly not effortless. Still, for many who feel stuck with no better options, it can be a smarter step forward than bankruptcy.

FAQs

1. Is National Debt Relief Legit?Yes — National Debt Relief is the real deal. The company is accredited by several respected organizations, including the American Fair Credit Council, the American Association for Debt Resolution, and the International Association of Professional Debt Arbitrators. That’s not just industry jargon — it means they follow strict standards for ethical debt settlement practices. They’ve also racked up tens of thousands of mostly positive reviews on sites like Trustpilot and the Better Business Bureau, which gives them an A+ rating. So while it’s smart to be cautious with any financial service, this one has the credentials to back it up.

2. What Exactly Does National Debt Relief Do?In a nutshell, National Debt Relief talks to your creditors for you — aiming to get you a better deal on what you owe. That could mean reducing your overall balance, asking creditors to drop late fees, or even pushing for lower interest rates. In some cases, they can help get your accounts reported as current once a settlement is made. The goal is to make your debt more manageable and help you settle for less than the full amount, without having to go it alone.

3. Does National Debt Relief Ruin Your Credit?Debt settlement through National Debt Relief will almost certainly ding your credit score — especially at first. That’s because part of the process involves pausing payments on your enrolled accounts while negotiations are underway. Those missed payments get reported as delinquencies, which can lower your score and stay on your credit report for up to seven years. That said, many people considering debt settlement already have struggling credit. And once the debt is resolved, it can be the first step toward rebuilding your financial standing.